The US-China trade dispute remains unresolved, casting a long shadow over global growth, corporate earnings and therefore "risk assets" such as equities and corporate bonds as a whole. While it can be argued that investors are now accustomed to the daily flow of tweets and headlines that often contradict each other in short order, getting a full grasp on the cost of the trade dispute itself remains elusive.

Much of the difficulty is linked to the basic uncertainty as to how long the trade dispute will actually last - and even more fundamentally – whether we will go back to the pre-dispute norm, which was characterised by the long term reduction in tariffs and the promotion of free trade? After all, tariffs are a form of taxation and these higher taxes reduce consumers' spending power, lowering GDP growth.

The latest batch of US tariffs on imports from China are different from earlier rounds. For one, they target a large number of consumer goods, including clothing and mobile phones. However these items will not be hit with punitive tariffs until after the critical year-end US holiday shopping season. While President Trump could theoretically change his mind and cancel the next round of tariffs, we expect them to be implemented nonetheless. This is largely because President Trump remains a popular leader according to opinion polls, but his popularity is split strictly along political party lines: Republicans approve of his policies and think the economy is doing well. Democrats tend to feel the exact opposite (despite the fact that US unemployment is very low at 3.6%, stock markets this year have been resilient and home prices are steady). Independent voters (those not affiliated with either major US party) appear to have a neutral view, and winning their support will likely be the key battle in 2020.

How can Independents be convinced to vote for President Trump? We suspect that the White House will announce another fiscal easing package, probably by 1Q20, to give the US economy a boost just in time for the November 2020 election. For these measures to be meaningful, he will require the cooperation of the Democrat-controlled House of Representatives. Therefore the question is, "Will Democrats oppose these steps?" In our view, if congressional Democrats stand in the way of a mini-stimulus, they will be vulnerable to attacks from Republicans who will charge that their opponents are putting partisan feelings ahead of what is good for economic growth. That would be risky from the Democrat's perspective; hence, we think they will grudgingly go along with this Republican plan.

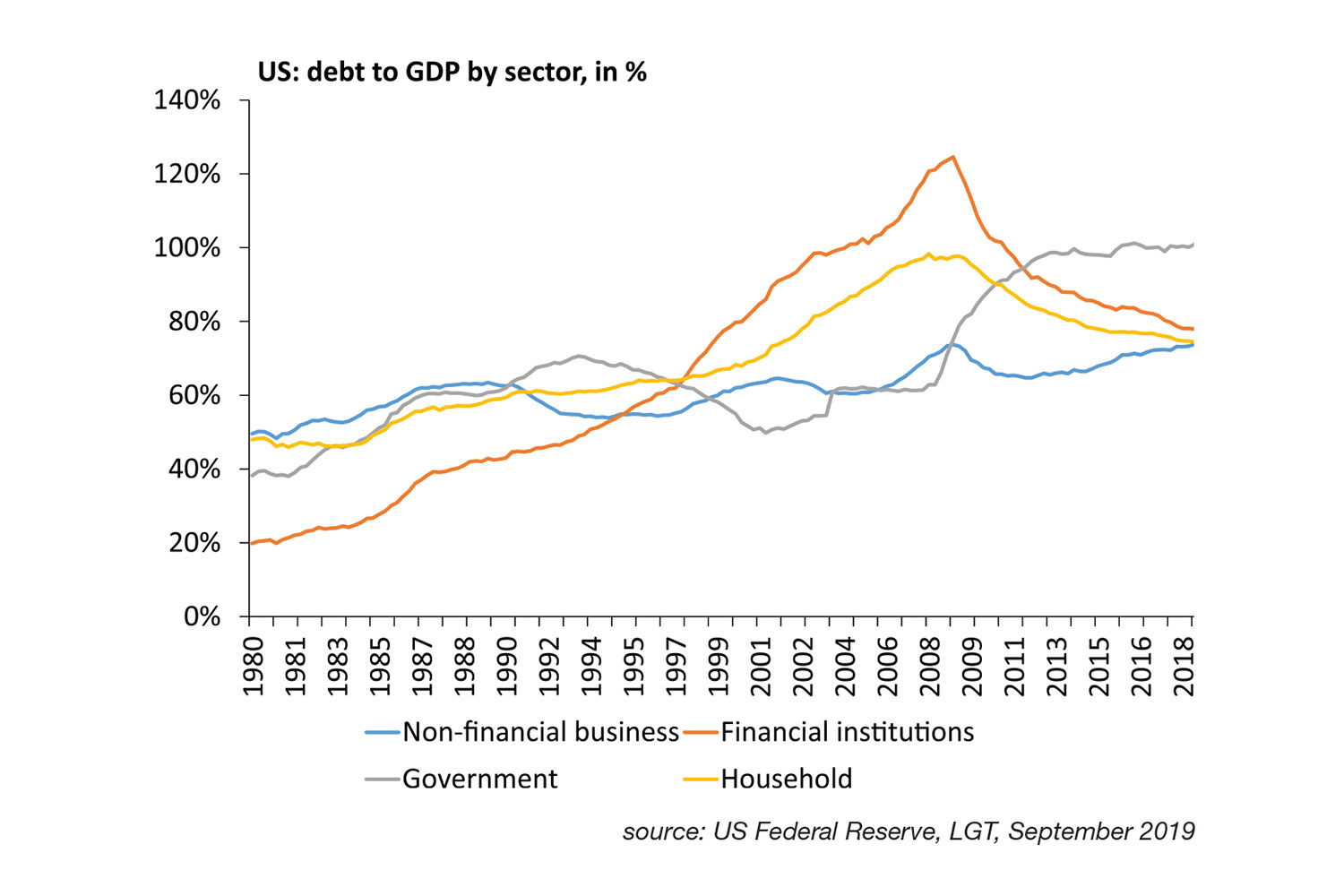

Can the US government afford more spending, given that the federal deficit has already increased substantially and government debt levels are surging? In short, yes. From the below chart we see that US households and financial institutions have de-leveraged whereas government debt has risen by around 20% of GDP since the end of the Global Financial Crisis. With interest rates falling, so too are borrowing costs of the US government. Furthermore, US government bonds still have a positive yield, meaning there is no shortage of buyers for US Treasuries in a world where negative-yielding sovereign debt is becoming increasingly common. That said, a mini-stimulus is not a substitute for resolving the US-China trade dispute, in our view. Investors may have to wait well beyond the 2020 elections for a meaningful de-escalation of tensions, not to mention a rolling back of punitive tariffs. We had originally assumed that the US and China would resolve their differences in 2019. A US mini-stimulus next year seems like a far easier bet to make.

The information contained in this article has not been reviewed in the light of your individual circumstances and is for information purposes only. It does not purport to provide investment, legal, taxation, or other advice and should not be taken as such. No person should act or refrain from acting on the basis of the content of this article without seeking specific professional advice.