The coronavirus has produced something new in economic history. Never before have governments tried to put swaths of national economies in an induced coma, artificially maintain their vital organs, and awaken them gradually.

Some past societies, such as medieval Europe, abandoned economic activities as people tried to escape plagues, and suffered heavy disruptions to their social order. In other pandemics, such as the flu of 1918, economic interactions continued with only limited quarantine measures, as authorities accepted contagion and deaths as the price of continuity.

Today, many nations are more willing--or feel more able--to try to have it both ways. Their hope is to press pause on the economy, save lives, and then press play again. If it works cleanly, it will be a testament to the flexibility of modern capitalism and the ingenuity of modern government. More likely, much will go wrong.

"We're in unknown territory. Inevitably there's a lot of guesswork," said Simon Tilford, an economist at Forum New Economy, a Berlin think tank.

The problem is that the economy has no pause button. Social-distancing measures, such as telling people to stay home and businesses to close unless essential, can suspend the buying and selling of most goods and services. But many costs keep on running. Households have rent or mortgages to pay, as well as bills for food and other necessities. Businesses have payrolls, debts and other fixed overheads. Banks owe money and so must collect it.

The conundrum of how to pay wages, rents and interest in the absence of sales has three kinds of answer.

People and businesses could live off their savings until the restrictions end. But many don't have enough reserves. The longer the health emergency lasts, the more people will run out of money.

The private sector could cut its outlays to match the commerce that is still permitted. But that raises the specter of mass unemployment and bankruptcies, the destruction of countless normally viable businesses, the scattering of workforces, and perhaps a lasting depression.

"There's a clear common societal interest in preserving jobs and companies from this external shock," said Christian Odendahl, chief economist at the Centre for European Reform, a think tank. "Our economic structure is a very complex machine, and its organization, the match between workers and firms, is difficult to replicate once it's gone."

To avoid such armageddon, the government can substitute for sales for a while, sending or lending enough money to cover wages, interest and other fixed costs. In theory, the state could preserve today's companies and jobs for months on end, provided it can borrow or print enough money and target the aid perfectly, and that people trust normality will return.

In practice, the outcome in many countries is likely to involve a mix of savings, slump and subsidies.

Government packages of fiscal and liquidity support are already huge: $2 trillion in the U.S. and hundreds of billions of dollars in Germany, the U.K. and France. European countries are focusing on subsidizing payrolls so that companies don't lay off their workers. The U.S. is offering forgivable loans to businesses that hold on to staff, but also expanding unemployment benefits and sending one-time checks to households. Many countries are delaying taxes and encouraging or paying banks to accept late payments on loans.

But politics has inevitably meant disagreement about how to target the aid, and how far to go in subsidizing the private sector. The U.S.'s aid package came too late to avoid a sudden jump in job losses last week.

"We're seeing unprecedented liquidity support in many countries, but the collapse of private consumption is so big that many firms will go under," said Mr. Tilford.

In the U.S. and Europe, there is debate over which sectors and companies deserve handouts, which parts of the private sector should be asked to absorb some of the cost themselves, and how to avoid pumping money into ailing companies that would have gone bust anyway.

There is also reluctance in some countries to borrow too much, only a decade after the global financial crisis pushed up public debts. That concern in particularly acute in Italy, which has both the world's deadliest coronavirus outbreak and fragile finances.

Italy's fiscal and liquidity measures of around €25 billion ($27.8 billion) are small compared with those of most other big European economies. Yet Italy's lockdown is among the most stringent outside central China, where the pandemic began, and is already weighing heavily on an economy that never fully recovered from the last financial crisis.

Rome's cautious economic response reflects its high national debt and fragile bond market, which in bad times relies on investors' trust that the European Central Bank would intervene to stop a rout. Italy, wanting more protection, is pushing for joint borrowing by eurozone members, but countries led by Germany and the Netherlands reject that.

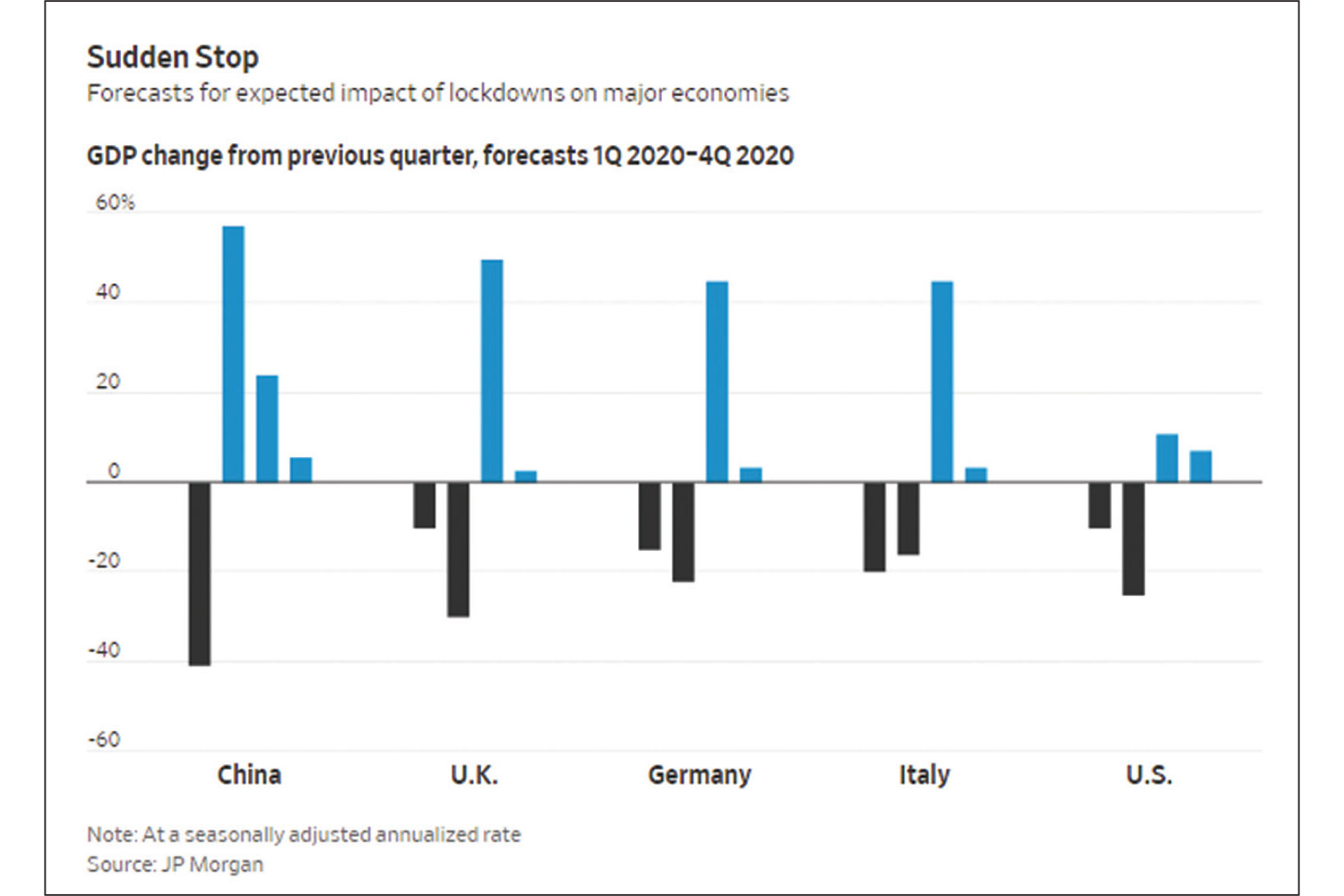

Bringing economies out of their induced comas will be slow. Countries don't want resurgent coronavirus outbreaks to force a second bout of lockdowns. Nobody knows yet how many months will pass before normal commercial activity resumes in full. For countries with large tourism sectors, such as Italy and Spain, losing the summer to continued restrictions would be another heavy blow.

If the operation succeeds, there will be the question of what to do about the large additional public and private debts. Forgiving loans to businesses that held on the workers could help the private sector to recover, but add to public costs.

High public debts, however, are nothing new in history. Experience suggests they are usually dealt with in several ways, from central banks buying and sitting on them, to forcing private banks and savers to lend cheaply to the government, to eroding their value through inflation.

A decade ago, European countries tried to pay down high public debts after the financial crisis with fiscal austerity. The economic pain and political backlashes felt around the continent had still not fully subsided when the pandemic struck, making a repeat less likely.