By the time readers read this article, Thailand still does not have a real government. But judging from the game being played, it is not too hard to guess which party will lead a new government.

However, it does not matter to me who gets to run the government because they will have the hardest time trying to prevent the economy from entering a recession or a crisis. The reason is that the Thai economy has no money and is almost as broke as the pre-Tom Yum Kung crisis of 1997.

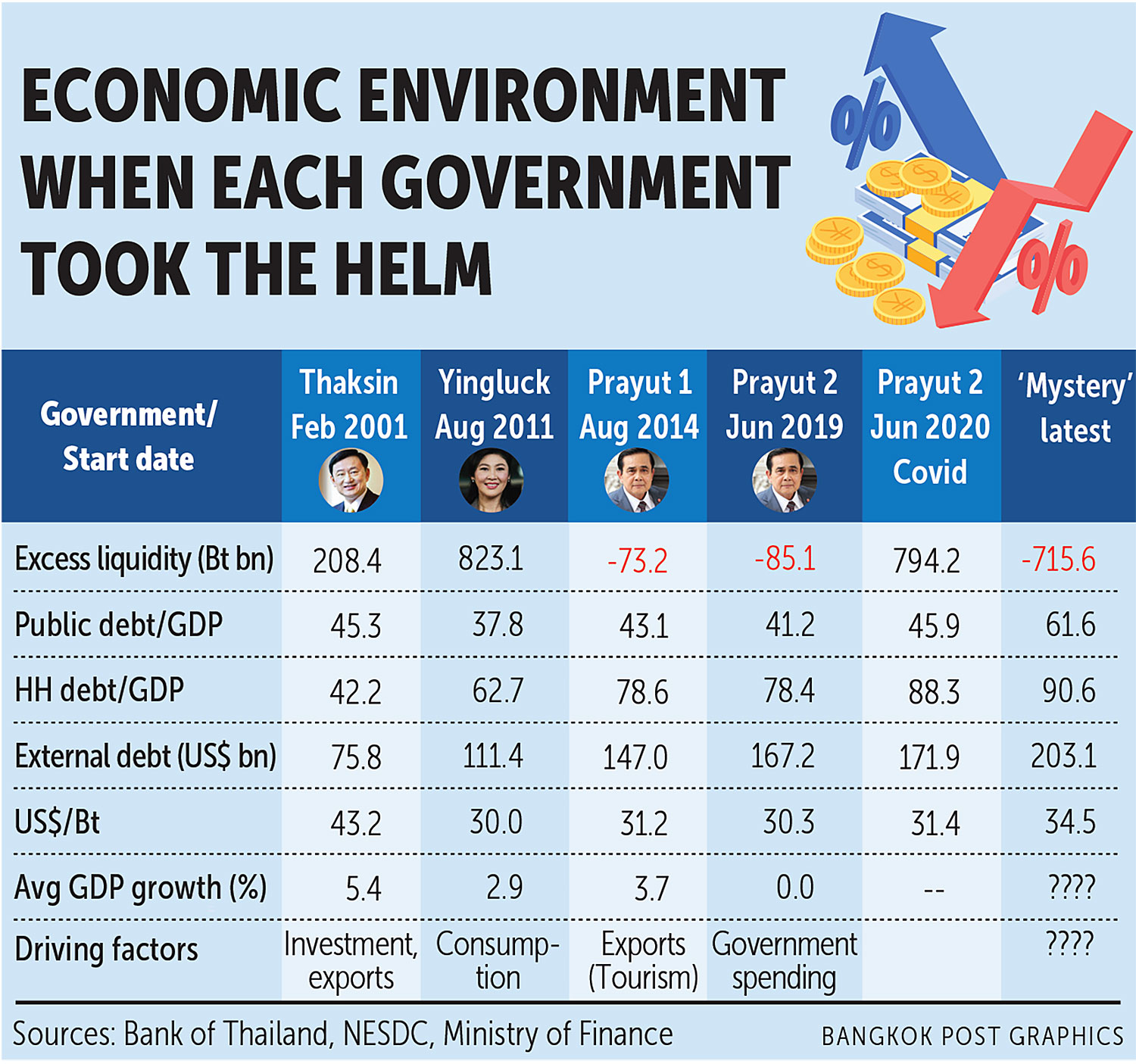

Readers do not have to believe me. Just look at the government figures in the graph below supporting this article.

The most important data is the first row of "excess liquidity", which provides cash for the government to stimulate the economy through public spending and for households to borrow to drive consumption.

All governments presented in the graph have some excess liquidity to start their administrations with or, at least, minimum negative excess liquidity. The concern is that the upcoming government will face the largest negative cash position in Thai economic history.

But this concern about the "largest negative cash position in Thai economic history" isn't entirely correct. The Thai economy experienced higher negative excess liquidity of 1.2–1.5 trillion baht before the Tom Yum Kung crisis in 1997. And that's exactly the reason why Thailand had a crisis that shocked the world.

For the benefit of the upcoming government, its economic team, and ordinary people like us, this article will explore economic policies utilised in each (selected) administration so as to learn from their successes/failures.

Let's begin with Prime Minister Thaksin Shinawatra's administration from February 2001 to September 2006.

Thaksin is the winner of the economic achievement award with 5.4% GDP growth. The secret of his success is attributed to an "undervalued" Thai currency. When he first entered office, it was after the crisis of 1997, and the baht was grossly undervalued. According to my calculation, the "right" value for the baht then was 38 baht per dollar. But it was 43.2 baht to the dollar in 2001 and further depreciated to 45.6 baht a few months later. This undervalued currency, coupled with his solid economic policies, lured investment to Thailand. Foreign direct investment (FDI) almost tripled. Also, exports earned double-digit growth from the cheap currency. In 2004, investment and export growth were 15.9% and 14.6%, respectively.

A high time for Thailand, indeed.

But, let me say again, Thaksin's policies were good, and an undervalued Thai baht played a key supporting role. When Thaksin left the office, the baht strengthened to 37 baht to the dollar.

The Thaksin government pushed the economy with an investment and exports-driven growth strategy -- the most admired strategy according to economic textbooks.

Years later, it was Yingluck Shinawatra's turn in government, and Thaksin's sister's economic performance was mediocre, with average GDP growth of 2.9%. With 30 baht per dollar, Thailand was no longer competitive and domestic demand needed to replace the external demand of FDI and exports. The situation got much worse after the floods of 2011. Her government needed to do something monumental to spur the flood-damaged economy. Then came the controversial rice subsidy scheme with a total cost of 881 billion baht. Not only did farmers get a big bonus, but workers were awarded a minimum daily wage increase from 215 baht to 300 baht, while consumers enjoyed a first-car policy with a maximum rebate of 100,000 baht per car.

Ms Yingluck's government pushed Thai economic growth through domestic consumption. The price? A high level of debt.

The government hid near to 9 billion baht of rice subsidy scheme debt at the Bank of Agriculture and Agricultural Cooperatives, while household debt increased by 15.9% of GDP as people bought new cars and other items. Luckily, she had 823 billion baht of excess liquidity and US$35.6 billion, equivalent to about 1 trillion baht, of foreign borrowing to finance her policies.

How about Prime Minister Prayut Chan-o-cha? He was prime minister twice, so I term it Gen Prayut I and Gen Prayut II. I must credit the man for being conservative with no major stimulus packages during his first administration. In fact, he was able to slightly lower public debt/GDP and household debt/GDP ratios while keeping the economy at a satisfactory level with a 3.7% growth rate.

I do not mean to rub it in, but Gen Prayut I's growth was significantly higher than Ms Yingluck's time, with no help from excess liquidity and household debts.

Much like Thaksin, Gen Prayut had a secret helper -- a booming tourism industry. The number of foreign tourists increased to 38.2 million in 2018. He could have pushed the economy further with tourist money by increasing government spending and encouraging more household debt. But a stable economy of 3.7% growth was fine with the man.

It is almost unfair to review the economic performances of Gen Prayut I's administration as the country and the world were hit hard by Covid-19. The number of incoming tourists was reduced from 40 million in 2019 to 0.4 million in 2021. The only reason why Gen Prayut was able to keep economic growth at 0.0% was because of large public spending and household borrowing. Public debt increased by 20.4% of GDP, and household debt increased by 12.2% of GDP.

This incredible amount of debt that saved the Thai economy during the pandemic could only happen for two reasons. First, the large inflow of foreign money in 2020. At that time, the US dollar was losing value, and investors searched for safe places to park money. Thailand was one of them, and 700 billion baht flew into Thailand within the first six months of 2020, and that was the 700 billion baht of excess liquidity shown in the column "Prayut II-Covid" in the table. Second, 30 billion dollars (1 trillion baht) of foreign borrowing.

The upcoming government will face the worst economic environment ever, not counting the pre-Tom Yum Kung crisis. Excess liquidity stands at negative 716 billion baht (and likely to be higher as capital still flows out from Thailand); public debt/GDP is 61.6% (and about 10% more is not yet officially recorded); household debt/GDP reaches 90.6% (and does not include informal debt of about half a trillion baht). How can one manage an economy under these stressful conditions?

Oh, and implementing the 10,000-baht digital wallet handout scheme, which some hope will push the Thai economy beyond 5% growth -- I don't want to be a party pooper but let me tell the economic team a disappointing theoretical fact. The scheme will only be effective if it is funded by new money such as foreign borrowing, the BOT printing money, and/or unused excess liquidity. If the scheme is self-financing, ie, funded by tax income and budget cuts, it will not be effective. Read more of Milton Friedman's books, and one will understand.

Can this lack of liquidity situation be mended? Hopefully, the new government will have a capable team of economists to fix the problem, or the Thai economy will risk facing a crisis.

My next article is not to be missed. The title will be something akin to "Why am I smelling Tom Yum Kung cooking in the kitchen?" and, of course, it's not a food article.